SplitPay Onchain Architecture

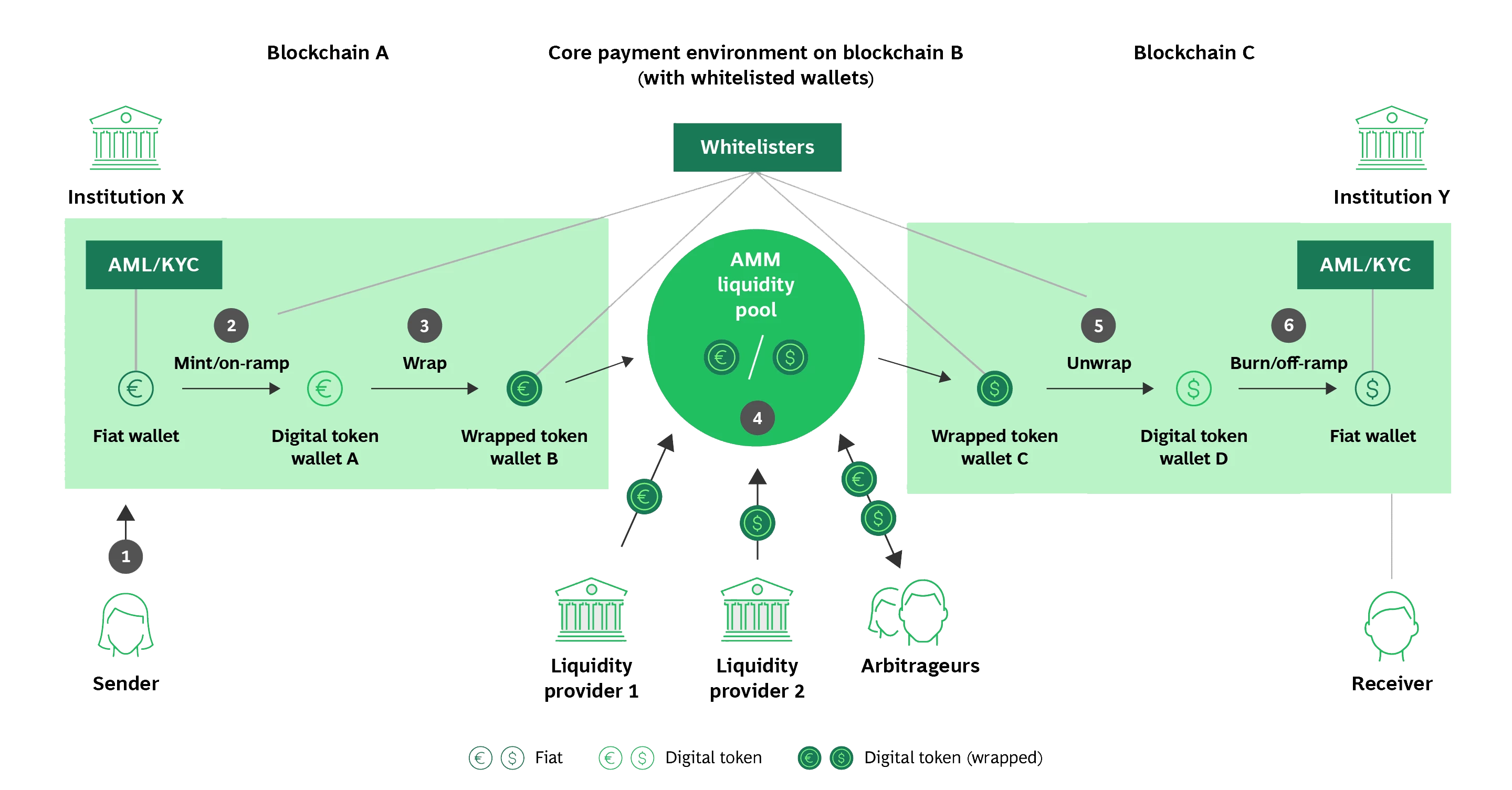

SplitPay Onchain operates as a decentralized settlement layer designed to resolve the latency and friction inherent in cross-border payments. Unlike traditional split-payment applications that rely on centralized ledgers and opaque banking rails, this system utilizes smart contracts to automate the division of funds across multiple recipients in real time. The architecture prioritizes transparency and finality, ensuring that every transaction is recorded on the blockchain rather than held in intermediate accounts.

The core logic resides in a smart contract that defines the split rules before funds are moved. When a user initiates a payment, the contract locks the assets and distributes them according to pre-agreed percentages. This eliminates the need for reconciliation by third-party processors and reduces the risk of fund misallocation. The system supports major stablecoins, allowing users to settle debts in digital assets that maintain a peg to fiat currencies, thereby mitigating currency volatility during the settlement window.

By removing the intermediary, SplitPay Onchain reduces the total cost of cross-border transactions. Traditional methods often involve multiple correspondent banks, each taking a cut and adding days to the processing time. In contrast, onchain settlements occur within minutes, with fees determined by network congestion rather than fixed banking surcharges. This efficiency is critical for businesses and individuals who require immediate access to split funds across international borders.

Real-time liquidity in cross-border flows

Traditional cross-border payments operate on legacy rails that prioritize security over speed, creating a structural delay between transaction initiation and final settlement. For creators and freelancers, this lag is not merely an inconvenience; it is a liquidity tax. Funds often remain trapped in correspondent banking networks for three to five business days, exposing recipients to foreign exchange volatility and restricting capital efficiency. SplitPay Onchain addresses this friction by leveraging onchain infrastructure to achieve near-instant settlement, effectively collapsing the settlement cycle from days to seconds.

The mechanism relies on stablecoin rails that bypass the SWIFT network's batch-processing limitations. By utilizing permissioned decentralized finance models, the platform ensures that liquidity is available at the point of transfer rather than relying on pre-funded nostro/vostro accounts that tie up capital. This shift transforms cross-border payments from a delayed administrative task into a real-time financial event. The result is a significant reduction in the cost of capital for recipients, who can deploy funds immediately rather than waiting for clearinghouse reconciliation.

This speed advantage is particularly critical in volatile markets. When settlement times stretch over several days, the exchange rate at the time of payment initiation may differ substantially from the rate at which the recipient finally accesses the funds. Onchain settlement locks in the value at the moment of transaction, eliminating this exposure. The platform’s architecture, supported by infrastructure providers like Fireblocks, ensures that these transactions are not only fast but also compliant with institutional-grade security standards, bridging the gap between the speed of digital assets and the reliability required for professional payouts.

Crypto treasury management for creators

Creators managing cross-border revenue streams face a fundamental friction point: the disconnect between on-chain earnings and off-chain operational costs. Traditional treasury management relies on manual reconciliation, where funds sit in fragmented wallets or stablecoin pools until a human operator initiates transfers. This latency introduces settlement risk and operational overhead that scales poorly as revenue complexity increases.

SplitPay Onchain addresses this by treating treasury management as a programmable logic layer rather than a series of discrete banking events. Instead of moving funds manually, creators define split rules that execute automatically at the point of transaction. This shifts the treasury from a reactive accounting task to a proactive, automated system. The result is a unified view of multi-currency assets where compliance and distribution happen simultaneously, eliminating the need for end-of-month reconciliation cycles.

To understand the operational shift, it is necessary to compare the mechanics of automated on-chain splits against legacy payment processing and manual bank transfers. The following comparison highlights the differences in settlement speed, reconciliation effort, and cross-border friction.

| Feature | Manual Bank Transfers | Legacy Payment Processors | SplitPay Onchain |

|---|---|---|---|

| Settlement Speed | 2-5 business days | 1-3 business days | Instant (block time) |

| Reconciliation Effort | High (manual entry) | Medium (API mapping) | Low (automated logic) |

| Cross-Border Friction | High (FX fees, SWIFT) | Medium (FX spreads) | Low (native stablecoins) |

| Compliance Tracking | Fragmented | Centralized but opaque | Transparent (on-chain audit) |

| Automation Level | None | Partial (webhooks) | Full (smart contract) |

The data indicates that while legacy processors offer some automation through webhooks, they still rely on centralized intermediaries that can freeze assets or delay settlements. Manual bank transfers remain the most labor-intensive option, requiring significant administrative time. SplitPay Onchain’s approach leverages smart contracts to enforce split logic immutably, ensuring that creators and collaborators receive their shares instantly and transparently, regardless of jurisdiction.

For creators, this means treasury management becomes less about chasing payments and more about strategic allocation. By reducing the friction of cross-border settlements, creators can reinvest capital faster and maintain liquidity across multiple currencies without the overhead of traditional banking infrastructure.

Onchain payments 2026 risk factors

Use this section to make the SplitPay Onchain decision easier to compare in real life, not just on paper. Start with the reader's actual constraint, then separate must-have requirements from details that are merely nice to have. A practical choice should survive normal use, maintenance, timing, and budget. If a recommendation only works in an ideal situation, call that out plainly and give the reader a fallback path.

The simplest way to use this section is to write down the must-have criteria first, then compare each option against those criteria before weighing nice-to-have features.

No comments yet. Be the first to share your thoughts!