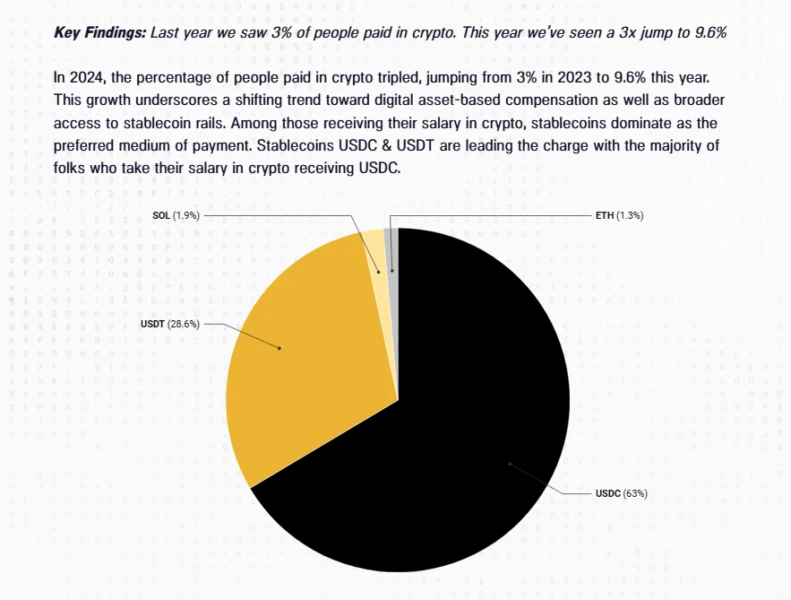

The onchain settlement shift

Traditional cross-border payment rails are structurally failing creators and businesses. The legacy SWIFT network, built for an era of physical letters and telex machines, introduces unnecessary friction into modern commerce. Transfers often take two to five days to settle, during which time funds are trapped in a web of correspondent banks. Each intermediary extracts a fee, and exchange rate spreads widen unpredictably, eroding the value of the payout before it ever reaches the recipient.

Onchain settlement addresses these structural inefficiencies by moving value transfer from a messaging-based system to a ledger-based one. Instead of relying on a chain of banks to verify and move funds, onchain systems settle transactions directly on the blockchain. This shift reduces settlement time from days to seconds or minutes, regardless of the countries involved. The cost structure also changes fundamentally, replacing layered banking fees with predictable network gas costs.

For cross-border payouts, this means real-time visibility and control. Businesses can track the exact status of a payment at every step, eliminating the black-box uncertainty of traditional wire transfers. Creators receive payments faster, improving cash flow and reducing the working capital tied up in transit. This efficiency is not just a convenience; it is a competitive advantage in a global market that demands speed and transparency.

The financial infrastructure is undergoing a quiet revolution. As more institutions recognize the limitations of legacy rails, the adoption of onchain settlement is accelerating. This shift is driven by the need for lower costs, faster speeds, and greater reliability in international finance.

How SplitPay Onchain settles cross-border payouts

Traditional cross-border settlements are often hampered by opaque banking rails, multi-day delays, and fragmented liquidity. SplitPay Onchain replaces this friction with programmable smart contracts that execute payments in real-time. By operating on public blockchains, the platform ensures that every transaction is immutable and transparent, providing a direct alternative to correspondent banking networks that rely on manual reconciliation.

The core mechanism relies on automated revenue splitting. Instead of sending a lump sum to a central account and waiting for internal distribution, funds are routed through smart contracts that instantly allocate percentages to multiple recipients based on predefined conditions. This is particularly valuable for global teams and B2B relationships where contractors, vendors, and partners operate in different jurisdictions and currencies.

For businesses receiving onchain revenue, the system consolidates fragmented income streams. As noted by Splits.org, onchain revenue often arrives as receipts in numerous assets; the platform turns that complexity into cleaner, stable-denominated deposits. This conversion reduces exposure to volatility and simplifies accounting, allowing finance teams to focus on growth rather than managing dozens of wallet addresses and exchange conversions.

The technical architecture supports the transfer of any token, ensuring flexibility for enterprises that hold diverse digital assets. Payees receive immediate notifications when payments are dispatched, eliminating the need for constant status checks. This level of automation not only accelerates cash flow but also ensures compliance with digital asset reporting standards, as every split is recorded on-chain for audit purposes.

To understand the market context for the assets typically used in these settlements, such as USDC or ETH, traders monitor real-time technical indicators.

Fee reduction analysis

Cross-border payments have long been defined by their friction, particularly regarding cost. Legacy banking rails, primarily relying on the SWIFT network, involve a chain of correspondent banks, each taking a cut for processing, compliance, and currency conversion. SplitPay Onchain disrupts this model by leveraging blockchain infrastructure to settle transactions directly, bypassing the traditional intermediary layer. This structural shift is where the claimed 60% fee reduction originates, representing a move from opaque, additive banking fees to transparent, protocol-based costs.

To understand the magnitude of this advantage, it is necessary to compare the cost structures of a standard $1,000 cross-border payout. Traditional wire transfers often carry flat fees ranging from $15 to $50, plus a hidden markup on the foreign exchange rate that can add another 2-3% to the transaction. In contrast, SplitPay Onchain fees are composed primarily of network gas fees and a minimal protocol fee. While gas fees fluctuate with network congestion, they are generally significantly lower than the fixed overhead of international banking corridors, especially when combined with the elimination of FX markups.

The following table illustrates the estimated cost difference for a single $1,000 payout, highlighting how onchain settlement reduces the total take rate.

| Method | Flat Fee | FX Markup | Total Cost | Total % |

|---|---|---|---|---|

| Traditional SWIFT Wire | $25 | $20 (2%) | $45 | 4.5% |

| SplitPay Onchain | ~$2 (gas) | 0% | ~$2 | 0.2% |

While the table above presents idealized figures for a standard transaction, real-world costs can vary. Network congestion may temporarily increase gas fees, but even during peak times, the cumulative cost rarely approaches the baseline fees of traditional banking. The primary savings come from the removal of the FX spread and the reduction of intermediary touchpoints. For high-volume businesses or individuals sending remittances regularly, these marginal savings compound significantly over time, turning a 60% reduction into a substantial operational advantage.

Creator payout workflows

For creators and agencies, the friction of cross-border payouts usually lies in the gap between earning and accessing capital. SplitPay Onchain collapses that gap by settling funds in real time. Instead of waiting for traditional banking rails to clear over several days, creators receive stable-denominated deposits directly into their wallets. This immediacy transforms volatile onchain revenue streams into predictable working capital.

The operational advantage is twofold: speed and simplicity. Splits allows businesses to send any token to contractors, with payees receiving instant email notifications upon receipt. This reduces the administrative burden of chasing invoices and reconciling multiple currency conversions. As noted in industry analysis, this process turns the "mess" of multi-asset receipts into fewer, cleaner deposits, effectively streamlining the path from revenue to liquidity.

Compliance is woven into this workflow rather than bolted on. By using onchain settlement, organizations can maintain transparent audit trails while adhering to regulatory standards. This is particularly valuable for US-based onchain businesses paying contractors across borders, as it provides a compliant mechanism that avoids the hidden fees and delays of traditional wire transfers.

To understand the impact of real-time settlement on cash flow, it helps to look at the volatility of the assets often involved in these transactions. The live price of Bitcoin illustrates the kind of market movement that makes stablecoin settlement attractive for consistent payroll and contractor payouts.

Implementation checklist

Integrating SplitPay Onchain requires aligning your existing financial infrastructure with on-chain settlement logic. This process moves beyond simple API connectivity to establishing trustless, real-time distribution of funds across borders. Follow these steps to ensure a compliant and efficient deployment.

Configure the smart contract parameters to reflect your specific payout needs. Determine the percentage or fixed amounts allocated to each beneficiary, including vendors, contractors, or partners. Ensure these ratios are immutable or governed by a multi-sig wallet to prevent unauthorized changes.

Link your treasury or operational wallet to the SplitPay Onchain interface. Select the settlement currency—typically stablecoins like USDC or USDT—to mitigate volatility risks during the cross-border transfer. Verify that your wallet supports the specific blockchain network where SplitPay operates.

Execute a small-scale test transaction to validate the end-to-end flow. Confirm that funds are split correctly, beneficiaries receive their portions in real-time, and on-chain receipts are generated accurately. This step is critical for verifying gas fee calculations and network compatibility before going live.

No comments yet. Be the first to share your thoughts!